Market value

Market value or OMV (Open Market Valuation) is the price at which an asset would trade in a competitive auction setting. Market value is often used interchangeably with open market value, fair value or fair market value, although these terms have distinct definitions in different standards, and may differ in some circumstances.

Market price

In economics, market price is the economic price for which a good or service is offered in the marketplace. It is of interest mainly in the study of microeconomics. Market value and market price are equal only under conditions of market efficiency, equilibrium, and rational expectations.

On restaurant menus, "market price" (often abbreviated to m.p. or mp) is written instead of a price to mean "price of dish depends on market price of ingredients, and price is available upon request", and is particularly used for seafood, notably lobsters and oysters

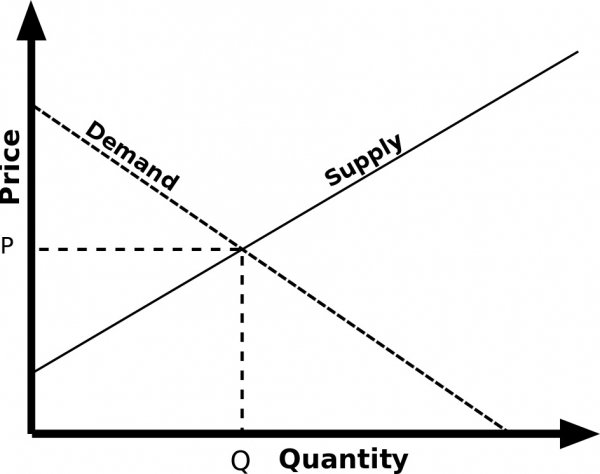

Market clearing

In economics, market clearing is a simplifying assumption made by new classical economics that in any given market, volumes always adjust up or down such that quantity supplied equals the quantity demanded. Market clearing is the process of getting there via price adjustment.

A market clearing price is the price of a good or service at which quantity supplied is equal to quantity demanded, also called the equilibrium price.

In simple terms, this means that markets tend to move towards prices which balance the quantity supplied and the quantity demanded, such that the market will eventually be cleared of all surpluses and shortages (excess supply and demand). The first version assumes that this process occurs instantaneously.

Economic equilibrium

In economics, economic equilibrium is a state where economic forces such as supply and demand are balanced and in the absence of external influences the (equilibrium) values of economic variables will not change. For example, in the standard text-book model of perfect competition, equilibrium occurs at the point at which quantity demanded and quantity supplied are equal. Market equilibrium in this case refers to a condition where a market price is established through competition such that the amount of goods or services sought by buyers is equal to the amount of goods or services produced by sellers. This price is often called the competitive price or market clearing price and will tend not to change unless demand or supply changes and the quantity is called "competitive quantity" or market clearing quantity

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good will vary until it settles at a point where the quantity demanded by consumers (at current price) will equal the quantity supplied by producers (at current price), resulting in an economic equilibrium for price and quantity.

The four basic laws of supply and demand are:

1. If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price.

2. If demand decreases (demand curve shifts to the left) supply remains unchanged, a surplus occurs, leading to a lower equilibrium price.

3. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price.

4. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.

Economic forces

Economic forces are the factors that help to determine the competitiveness of the environment in which the firm operates.

These factors include:

1. Unemployment level

2. Inflation rate

3. Fiscal policies

4. Government changes etc.

These factors determine an enterprise’s volume of demand for its product and affect its marketing strategies and activities. The economic system is made up of three main steps. The first one being production and then there is distribution of the produced goods and then the last step is consumption of the same. Now all this is possible because of two factors- Human resource and Natural resource.

Natural resources include the raw material which is generally used in the production process, and human resources help to convert the raw materials to finished products which are then ready for distribution.

Comments 0